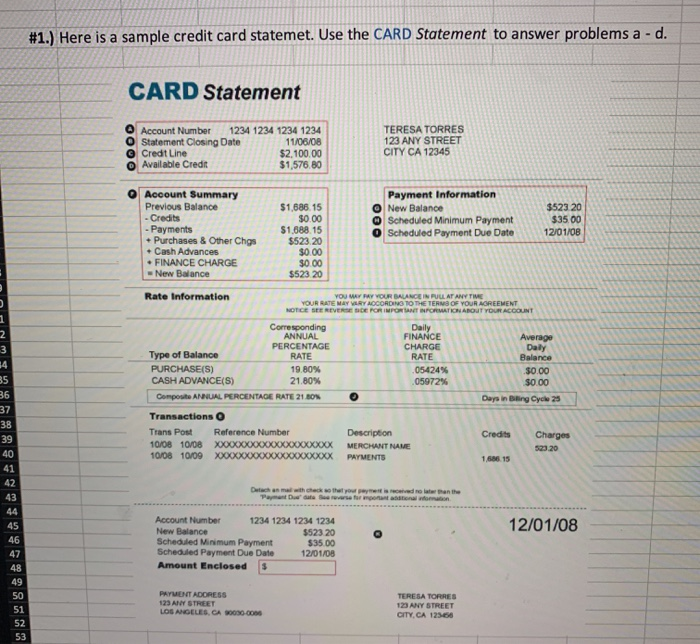

Effective Strategies for Managing Credit Card Debt

Credit card debt can feel overwhelming, but there are proven strategies to regain financial control. This guide explores practical approaches including debt consolidation, balance transfers, and budgeting techniques that can help you systematically reduce your debt burden. Whether you're dealing with $5,000 or $50,000 in credit card debt, understanding your options is the first step toward financial freedom.

Credit card debt affects millions of Americans, creating financial stress and limiting opportunities for wealth building. If you're struggling with mounting credit card balances, understanding the available strategies can provide a clear path toward debt freedom. This comprehensive guide outlines practical approaches that have helped countless individuals regain control of their finances.

Debt Consolidation Options

Debt consolidation involves combining multiple credit card balances into a single loan with potentially lower interest rates. This approach simplifies your payments and can reduce the total interest you pay over time. Personal loans from banks or credit unions often offer fixed interest rates that are significantly lower than credit card APRs, making them an attractive option for debt management.

Balance Transfer Strategies

Credit card balance transfers can provide temporary relief from high interest rates. Many credit card companies offer introductory 0% APR periods on balance transfers, typically lasting 12-18 months. This window allows you to focus on paying down principal without accruing additional interest. However, it's crucial to read the fine print regarding transfer fees and what happens to the interest rate after the promotional period ends.

Budgeting and Payment Planning

Creating a realistic budget is fundamental to debt reduction. Start by tracking your income and expenses to identify areas where you can reduce spending. The snowball method involves paying off smallest debts first for psychological wins, while the avalanche method targets highest-interest debts first for maximum financial efficiency. Choose the approach that best matches your personality and financial situation.

Seeking Professional Guidance

Credit counseling agencies can provide valuable assistance in developing debt management plans. These nonprofit organizations work with creditors to negotiate lower interest rates and create structured repayment plans. For more severe situations, debt settlement companies may negotiate with creditors to accept less than the full amount owed, though this approach can negatively impact your credit score.

Long-Term Financial Habits

Beyond immediate debt reduction, developing healthy financial habits is essential for preventing future debt accumulation. This includes building an emergency fund to cover unexpected expenses, using credit cards responsibly by paying balances in full each month, and regularly reviewing your financial goals. Financial education resources, including those from the Consumer Financial Protection Bureau, can provide ongoing support for maintaining debt-free living.

Successfully managing credit card debt requires commitment and strategic planning, but the financial freedom gained is well worth the effort. By implementing these strategies and maintaining disciplined financial habits, you can overcome credit card debt and build a more secure financial future.